Prior to discussing how to calculate operating leverage, lets define it. Operating leverage is a cost-accounting formula that measures the degree to which a firm or project can increase operating income by increasing revenue.

In companies with a high operating leverage degree, a large proportion of the company’s costs are fixed costs. In this case, the firm earns a large profit on each incremental sale, but must attain sufficient sales volume to cover its substantial fixed costs. However, earnings will be more sensitive to changes in sales volume.

In a firm with a low operating leverage degree, a large proportion of the company’s sales are variable costs, so it only incurs these costs when there is a sale. In this case, the firm earns a smaller profit on each incremental sale, but does not have to generate much sales volume in order to cover its lower fixed costs.

Advantages of Operating Leverage.

- Operating leverage helps to analyze the type of business, if high, it means the company is capital intensive.

- It helps the business to calculate the break-even point.

- It helps the firm to understand the level of operating risk.

- This concept helps firms decide on a better sales strategy.

Disadvantages.

- High operating leverage makes the firm more sensitive to changes in revenue.

- The firm has to earn high revenue to break even, which puts pressure on the operation process.

- A business with high operating costs finds it difficult to obtain financing easily.

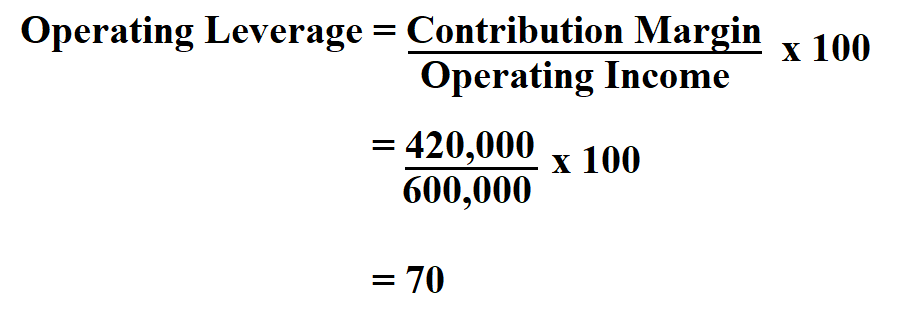

Formula to Calculate Operating Leverage.

The contribution margin is the difference between total sales and total variable costs.

Example:

If the contribution margin is $ 420,000 and the operating income is $ 600,000. Calculate the operating leverage.

Therefore, the operating leverage is 70%.

{kind=link}

{kind=link}